Product vs Distribution

“The battle between every startup and incumbent comes down to whether the startup gets distribution before the incumbent gets innovation.”

This take from Alex Rampell did encapsulate the intricate relationship between two of the most important aspects when looking at any business - product, and distribution.

In today’s post, let's explore some schools of thought on product vs distribution.

Product vs Distribution, What’s more important?

Let's say you’re a founder and you can only choose one between two options:

Either having a distribution advantage or having a product advantage over your competitor?

Which advantage would you choose?

Marc Andreessen’d chose distribution. For him, distribution is more important, specifically owning a distribution advantage is way more valuable than owning a product advantage. The reason is that for most verticals, distribution is harder to commoditize - there are only a few distribution channels in the world for any given industry, while the product can usually be easily copied.

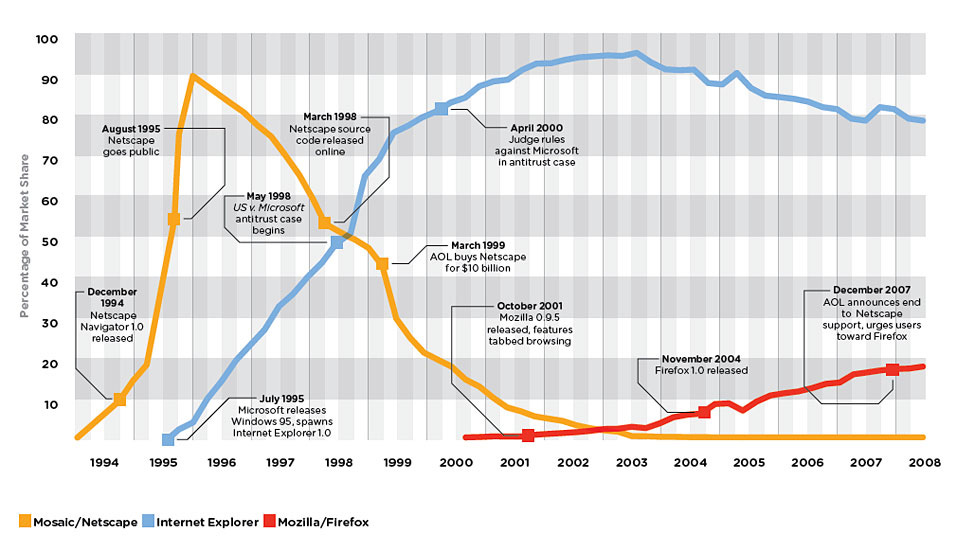

Of course, Marc knows what he’s talking about since he experienced this firsthand in the first Browser War between Netscape and Internet Explorer. It was a classic tale of a startup with a great product advantage being crushed by an incumbent with a distribution advantage.

In case you don’t know Marc Andreessen, long before he found a16z, he was the mind behind our first web browser - Mosaic, which later changed to Netscape. When he launched Netscape in 1995, it was an instant hit. In fact, it took Netscape just more than a year to go from the launch of its first version to its IPO event, which was later on considered the starting hallmark of the dot-com bubble era. As you can see in the chart below, Netscape created and then totally dominated the web browser market until 1995, that was when Bill Gates came in and used his distribution power - the Windows 95 OS to crush it.

As you know, Windows was the most popular OS at the time and still is today. What Microsoft did with Internet Explorer was basically copy Netscape’s product and then bundle it as the default browser for Windows 95. While people had to pay Netscape to be able to install its browser, Internet Explorer was completely free to download, and most importantly, it was preinstalled as the default browser for any new Windows 95 users.

With that context in mind, who do you think would win this war?

Of course, it was Internet Explorer. By piggybacking Windows 95’s growth, Internet Explorer enjoyed a far superior distribution advantage over Netscape.

Now, did you see why Marc chose distribution advantage over product advantage? This insight is further validated by his experience later on as a VC. He shared similar takes in an interview with Elad Gil

“The general model for successful tech companies, contrary to myth and legend, is that they become distribution-centric rather than product-centric. They become a distribution channel, so they can get to the world. And then they put many new products through that distribution channel.” - Marc Andreesseen

Nearly 30 years later, Microsoft is still aggressively following the "copy & bundle" playbook. The most recent victim was Slack, in its battle with Microsoft Teams.

Thanks to the advantage of owning the distribution channel, Teams was bundled together within the Office 365 package. It took Teams just over 2 years to catch up with Slack's product lead before completely crushing Slack in 2020 when it hit 75 million DAU - 6 times higher than Slack's 12 million DAU.

The explosive growth of Teams forced Slack to change its strategy. At the end of 2020, Slack announced that it had reached an agreement to be acquired by Salesforce. This is a wise move for Slack to counterbalance Teams in terms of distribution muscle. Thanks to Salesforce’s existing distribution network of 150,000 enterprise customers, Slack will be "bundled" and sold together within Salesforce's product suite, thereby partly being able to compete more fairly with Teams.

Now you must have somewhat understood what Marc meant at the beginning, right? The advantage of having a product lead can sooner or later be copied, it’s the advantage of owning the distribution channel that endures.

Chinese Distribution Mindset

There are many examples of great startups leveraging their distribution advantage incredibly well. Meituan is probably the first name that comes to my mind.

In case you don't know, Meituan is the 3rd largest tech company in China, just behind Tencent and Alibaba. This juggernaut offers all kinds of services from food delivery, car-hailing, grocery shopping, hotel booking, movie ticket buying, ecommerce marketplaces to B2B fintech... An easier way to visualize the sheer scale of Meituan is to imagine there is a startup that provides the services of Doordash, Yelp, Opentable, Groupon, Uber, Instacart, Expedia, Airbnb, Amazon, Square ... all in one single mobile application.

Okay, so with such a variety of products where did they even start?

Their strategy is simple: Enter and dominate verticals with high-frequency usage first, then expand from there.

(Frequency here refers to the number of times the user uses the product / opens the app in a certain time period. For example, a chat application like Messenger - opened by the user many times a day will have a higher frequency than a food delivery app like UberEats - which is only opened 1-2 times per day. Similarly, Food Delivery apps then have a higher frequency than Travel Booking apps like Airbnb which is only used 1-2 times per year).

Ok, but why did Meituan choose to start with high-frequency verticals first?

The answer is that high-frequency apps form users’ habits. And once your app has a certain place in the user’s top of mind, you now own a superior distribution channel that can be leveraged to cross-sale many other products/services.

Starting with a high-frequency vertical first and then subsequently layering on other lower-frequency verticals is much easier than the other way around. This is probably the most important mental model to understand China’s consumer tech market. As Wang Huiwen - the co-founder of Meituan once shared, almost all big tech giants in China follow this playbook faithfully.

This’s why Meituan started with food delivery since you need to eat 3 times per day -which is pretty high frequency compared to other services. Then only after having nailed food delivery that Meituan expanded to other services with lower frequency such as movie tickets, travel ...

Similarly, Pinduoduo’s founding story exemplifies the same strategy. The reason that they chose to start with the niche of selling vegetables/fruits first - was also because of the "high-frequency usage" nature of these products.

Imagine the number of times you need to buy vegetables in a month compared to the number of times you buy high-tech appliances. Obviously, you buy more vegetables, right? Yeah, that's why Pinduoduo chose to sell fruits/vegetables (high-frequency) first and then gradually expanded to now sell technology, electronics appliances (low-frequency), and all kinds of other stuff, but not the opposite direction of starting with the technology/electronics first and then expand to sell vegetables.

That’s also why Wechat has been so successful in China since its native product - messaging is so inherently high-frequency - which is used many times per day by users. As WeChat became “the top-of-mind app” in China, Tencent knew better than anyone how to take advantage of its distribution channel.

But instead of directly copying or acquiring then bundling and pushing down its own distribution channel as these Western juggernauts usually do, Tencent decided to turn WeChat into a distribution factory by opening up the WeChat Mini Program allowing other developers to build apps on top of WeChat.

From there, Tencent selects promising startups that are using WeChat as their main distribution channel to back with its investment arm. From Pinduoduo, Didi to Meituan and a host of other startups built on the Mini Program, Tencent always has a big piece of the pie.

At first glance, these two approaches may seem different, but in essence, they are the same. Whether directly coping/acquiring like in Microsoft, Salesforce’s playbook, or indirectly through investments like Tencent, these giants are all following the same strategy of being "distribution-centric" as Marc Andreessen noted.

For them, the distribution channel is their biggest asset, not any single product.

The strategy of starting with high-frequency verticals first is also being replicated by many other startups in the U.S. and other regions.

Turner Novak described JOKR’s (a quick commerce startup) ambitious plan to expand, starting by capturing the grocery market first due to its repetitive consumer behavior.

Capturing a repetitive consumer behavior like ordering groceries allows them to layer on other products over time. This could include, but not be limited to, everything from consumer payments, meal delivery, travel, streaming, healthcare, gaming, financial services, and products for their merchants and suppliers. This expansion into other product lines is generally the holy grail of any consumer internet platform as highlighted in Postmates Series B deck.

Super App’s Unit Economics

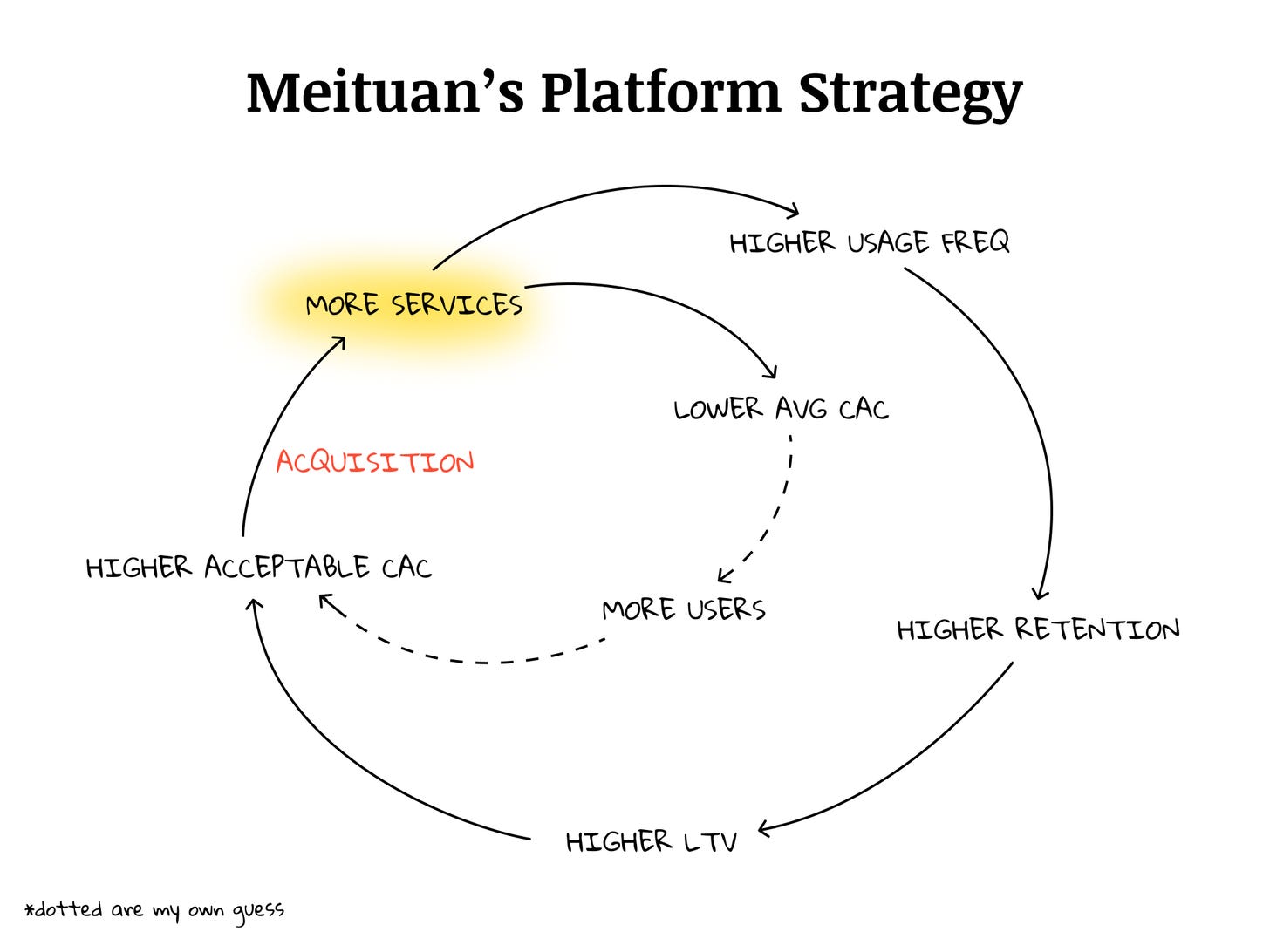

Another advantage of “distribution-centric” companies going in the direction of becoming Super-App by providing many products and services in the same app as Meituan did is that it creates a special competitive advantage in unit economics.

How?

Simple: Cross-selling multiple services increases users’ LTV => Once your LTV is much higher than your competitors, you can tolerate a much higher CAC than your competitors => You can be more aggressive than your competitors when it comes to acquiring users. Another way to think about this is that CAC is like a fixed cost, therefore it'll be very costly if you just offer one single service to your users. But if you offer multiple services in the same app, that fixed cost of CAC is kinda divided between these services.

Take a specific example. If we assume that the average LTV of the food delivery industry in China is $100 per user, then Meituan's competitors that only operate in the food delivery industry like Ele.me cannot accept a CAC greater than $100.

However, with Meituan, because they not only deliver food but also offer car-hailing, grocery shopping, hotel booking, movie ticket buying… all the revenue from these sources adds up to a huge LTV per Meituan user. Let's say that after adding up, we reach a total LTV per user of $300. This makes acquiring users with CAC > $100 acceptable to Meituan. Because of their scale, they can accept to outspend the competitors while still enjoying a profitable level of unit economics.

Likewise, Meituan's competitors that only operate in a single vertical usually suffer when competing with them. For example, in the travel-booking industry, although Meituan entered the market many years later than its competitors, Meituan has already surpassed C-trip to become the largest travel-booking platform in China.

This is also the reason behind Meituan's decision to buy Mobike - the bicycle-rental startup, for the sole purpose of using this application as a channel to "acquire users" for the Meituan super app.

When asked about the logic to make the decision to buy Mobike - which was still losing a lot at that time, Wang Huiwen frankly shared - Meituan was willing to lose money on Mobike because they will make money later on from other services of Meituan. In other words, basically, Meituan only considered the acquisition of Mobike as buying a distribution channel to be able to bring their other services to the new users.

“When an entire industry (bike sharing) may become a means of acquiring users for another industry (local services), can you still expect this industry to be profitable?”

Wang Huiwen - Cofounder of Meituan

With the fundamental rule of consumer tech that CAC always increases over time, the scale advantage of having a high LTV as a super app, thereby being able to tolerate an incredibly high CAC compared to its competitors will continue to be a powerful weapon of Meituan in the future.

Besides, as the Meituan app offers multiple services, the user uses it more often => higher frequency => higher retention.

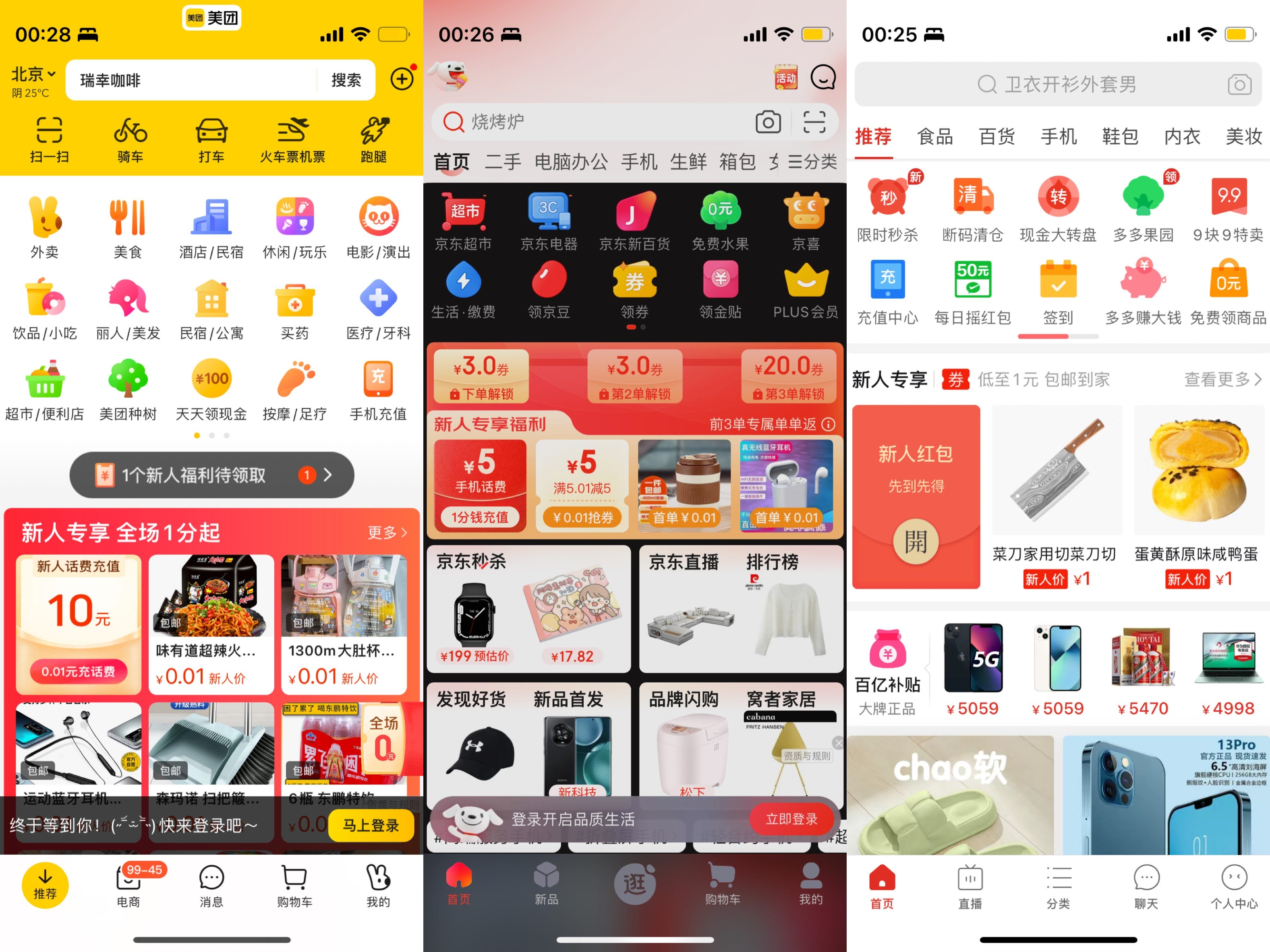

These flywheels of positive feedback loops gave Meituan a specific advantage over its competitors which only operate in a single vertical. Similarly, other giants in China like JD or Pinduoduo are also pursuing the same playbook of becoming a SuperApp, below are my screenshots of these 3 apps not long ago.

It’s hard to find the difference between them 🤣🤣🤣

Not only in China but the Super app model has also now been pursued by many startups around the world, especially in Southeast Asia. If you open Tiki, Zalo in Vietnam, you will see a bunch of other services offered inside. However, to reach a scale like Meituan, I think it will take a lot of time.

The logic regarding better unit economics of the Super app model is clearly undisputed, the only question we need to answer is consumer behavior.

China is a different consumer tech universe from the rest of the world. Users there have formed a habit of using super apps. They like using ride-hailing, ordering food, and buying goods… all in the same app. This is not true in most other markets, where users will usually use one app for each service. Imagine Grab opening a hotel booking service, how many people do you think will actually open the Grab app with the purpose of doing that in mind?

Similarly, I personally have never used any service in the mini program of Tiki or Zalo. This view is subjective because I don't have specific data on the exact percentage of users who actually interact with these programs, but I highly doubt that this number is significant.

Wedge and Distribution

Building a distribution-centric company seems to be a great playbook that has been pursued by many big techs. Elad Gil shared the same perspective as Marc.

Since focusing on product is what caused initial success, founders of breakout companies often think product development is their primary competency and asset. In reality, the distribution channel and customer base derived from their first product is now one of the biggest go-forward advantages and differentiators the company has.

This pattern of distribution as moat and competitive advantage was used ruthlessly by the prior generation of technology companies. Microsoft bought or built multiple franchises including Office (Word, Powerpoint, Excel were all stand-alone companies or market segments), Internet Explorer, and other products and then pushed them down common business and consumer channels. Cisco has purchased dozens of companies that were then repositioned or resold to their enterprise and telecom channels. 1 SAP and Oracle have exhibited similar patterns of success.

Successful startups usually have to, first, dominate a niche - usually called a wedge, then from that stronghold expand further. What your wedge is, aka your initial positioning in the market, has important implications on your distribution advantage and expansion plan later on.

Because different companies with different wedges in the same market will expand and eventually compete with each other, it’s important to keep in mind that not all wedges are created equal. This leads to the corollary - not all distribution advantages are the same.

In my opinion, the best wedge is being the foundation of a value chain.

As in the Microsoft vs Netscape case, Microsoft owned Windows - the foundational layer under Netscape. Similarly, companies with the best positions in the Crypto industry right now to expand are exchanges like Coinbase, Binance. Since they’re on the very top of the food chain by owning the users, they can continue to layer many other services on top such as Crypto payment, NFT marketplace… all thanks to their initial wedge as the on-ramp channel to anyone who wants to enter the crypto world. Similarly, Shopify can build Shop Pay to compete directly with Stripe since Shopify is the foundation that Stripe integrates into and they own the distribution channel to merchants.

=> Your wedge matters, especially in the long-term expansion later on.

Commoditization of Products makes Distribution even more important

You can see Marc's take on “distribution is hard to be commoditized while product is” especially obvious in cross-border Ecommerce.

As I mentioned in my writeup about Thrasio and Ecommerce Aggregator, the whole cross-border E-commerce stack has now been commoditized. From product sourcing, warehouse, logistics to website builders.

10-15 years ago, if you own a vertically integrated brand, it was a moat that not many people can afford. But now, it’s no longer the differentiator. Everything has been made easy. It’s so easy that virtually, everyone, anywhere in the world can create an e-commerce brand on Amazon, or Shopify from scratch, within a day. Since all of the layers underneath have been commoditized, the only thing left to differentiate between brands is the distribution or in this case performance marketing - specifically Amazon/Facebook/Google ads.

As performance marketing becomes the hardest part of the cross-border commerce stack => whoever is great at this now becomes the winner and owns the value chain.

That’s why Thrasio started initially as a conversion marketing agency, they’re so good that they decide to integrate backward to own the whole stack as an Ecommerce Aggregator.

It made a lot of sense though, as Keith Rabois said “if you can solve the hardest part of the value chain, there is no reason not to expand and own the whole stack”

Distribution-led thinking

The most extreme version of distribution-led thinking is Reid Hoffman’s saying:

I've discovered a distribution advantage. What product can I deliver with it?

This take captures the essence of the distribution-led mindset. Usually, we think about the product first and then think about the distribution later, Reid encouraged us to reverse this process. Instead, think about the distribution advantage that you might have first then think about what product you can build/acquire/invest in to leverage that.

A vivid example illustrating this might be the symbiosis between Tencent & Pinduoduo. Basically, Tencent had the distribution advantage of personal connections in its Wechat’s group chats which can be leveraged to build social commerce products. From Tencent’s investment perspective, this was a great synergy between Wechat and Pinduoduo, that’s why Tencent backed Pinduoduo.

From a founder’s perspective, if you want to copy PDD’s product but your country doesn’t share the same distribution similarities and user behaviors as in China then it could hardly work. That distribution advantage is unique and only works in China. That’s why social commerce startups in other parts of the world like Meesho in India, or Elenas in LatAm follow a totally different playbook compared to PDD as they don’t share the same distribution landscape as PDD did.

Probably the most interesting example of this take is McKinsey. The prestigious consulting firm is leveraging its distribution to Fortune 500 clients by acquiring SaaS companies, bundling them together into a suite of products that are later sold alongside their consulting services. Over the last 5 years, McKinsey has acquired 10+ companies and created McKinsey Solutions - the business unit that’s going to drive $100M+ ARR.

As Shaan Puri shared - “It wouldn’t surprise him if McKinsey builds a $25B+ software portfolio over the next 10 years”. All of this starts with its distribution advantage - the direct relationship with the clients.

Conclusion

Those are lessons that I’ve learned about Product vs Distribution, the yin and the yang of any business. I hope you enjoyed it as much as I did.

I’m also curious about how well these judgments can be applied to the actual business settings in Vietnam, therefore, if you have any insights into this, you’re more than welcome to reach out to me.

Finally, here’s one last take as a bonus before we finish. This old saying has almost become a cliche but it still resonates with me every single time.

That’s all. Thanks for reading and see you soon.

Cheers!!

Minh

Further readings:

High Growth Handbook - by Elad Gil

#007 - Product Management Lessons by Meituan Co-Founder - by China Playbook

Meituan - by Acquired Podcast

Picking a wedge - by Lenny Rachitsky

Reid Hoffman: The Network Philosopher King - by Starting Greatness Podcast

Cảm ơn anh Minh, bài viết rất hay và dễ hiểu ạ!

Tự nhiên em nghĩ đến case của Netflix và Disney+ (thực ra em chưa tìm hiểu kỹ đâu nhưng em cứ phát biểu luôn vậy haha :D ). Em thấy Netflix đang có lợi thế về distribution qua việc được cài mặc định trên hầu hết các dòng Smart TV. Disney+ thì chưa. Nhưng Disney+ đang lấy lại thị phần từ Netflix rất nhanh nhờ vào việc phát triển Product, qua Marvel series, Pixar movies và nhiều phim khác được chiếu độc quyền trên Disney+

Anh có dự đoán nào về chiến lược cũng như tiềm năng phát triển trong thời gian tới của 2 cty trên không ạ?

Ngoài ra, anh phân tích case của Disney+ và Netflix như thế nào dưới góc độ Product và Distribution ạ? Bởi thực ra em cũng nhìn nhận Netflix và Disney+ chính là những distribution chanel cho các sản phẩm phim của họ ạ.

Cảm ơn anh ạ!

Bài viết hay quá anh Minh ơi, em follow anh từ case anh viết về PDD. Em cũng muốn hỏi anh những source nào anh đọc về những model start up hay vậy ạ. Thanks anh